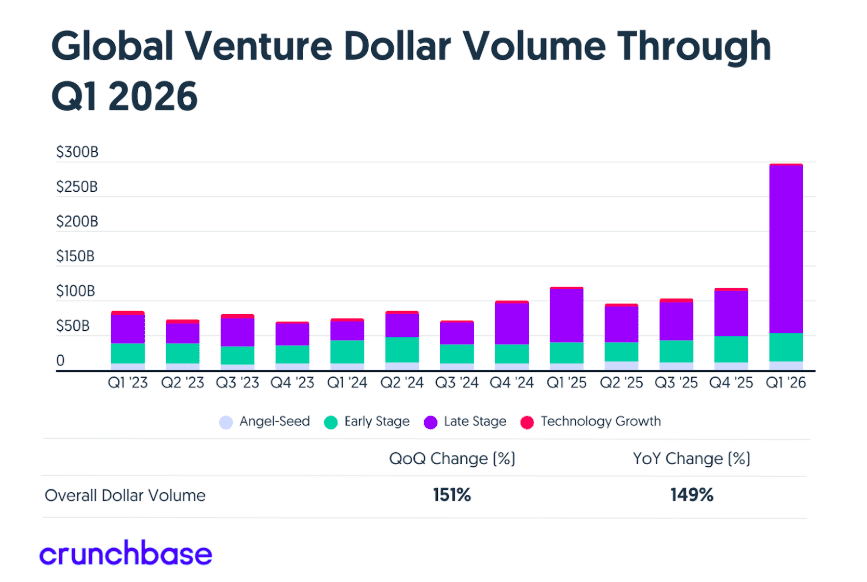

Global venture investment surged to a record of nearly $300 billion in the first quarter of 2026, fueled by “unprecedented” spending on AI compute and frontier labs, according to Crunchbase.

Investors poured $297 billion into roughly 6,000 startups worldwide during the quarter, about a 150% increase both quarter over quarter and year over year. It is the highest level of venture funding ever recorded for a single quarter and accounts for nearly 70% of all venture capital invested in 2025.

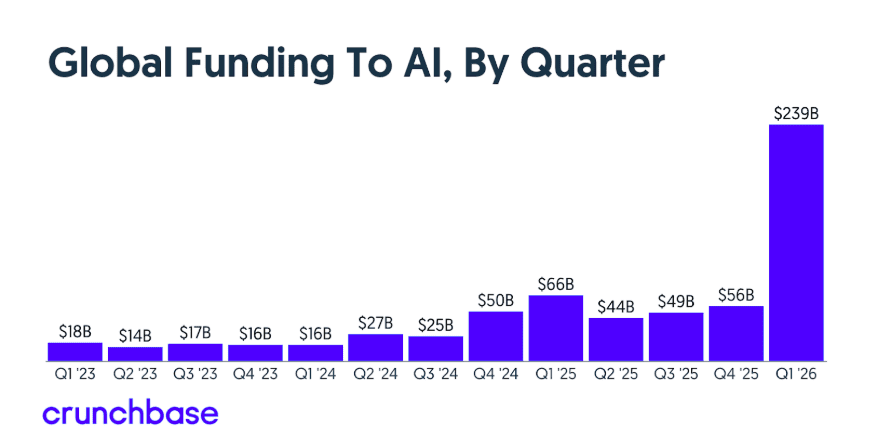

AI companies captured 81% of the funding in the quarter.

The surge was driven primarily by outsized investments in AI, particularly in a small group of U.S.-based companies. Four of the five largest venture rounds in history were completed during the quarter, including $120 billion raised by OpenAI, $30 billion by Anthropic, $20 billion by xAI and $16 billion by Waymo. Together, those deals accounted for $186 billion, or 64% of total global funding.

On March 31, OpenAI closed its $122 billion funding round for a post-money valuation of $852 billion. OpenAI, Anthropic, xAI and Waymo closed four of the five largest ever funding rounds in the quarter.

Overall, AI companies captured $239 billion in funding in the quarter. That is a sharp increase from the previous record set in the first quarter of 2025, when AI accounted for 55% of funding.

An additional 10 startups raised funding of $1 billion or more each in the quarter, from sectors including generative and physical AI, autonomous vehicles, semiconductors, data centers, robotics, defense, and prediction markets, according to Crunchbase.

The concentration of capital in a handful of companies drove a sharp rise in startup valuations. The Crunchbase Unicorn Board added $900 billion in value, the largest quarterly increase on record.

Funding was heavily skewed toward the U.S., where startups raised $247 billion, or 83% of global venture capital. That is up from 71% a year earlier and significantly above historical norms. China ranked a distant second with $16.1 billion, followed by the United Kingdom with $7.4 billion.

Most of the increase came from late-stage deals. Late-stage funding reached $244 billion, up 203% year over year, with $232 billion going to 157 companies that raised $100 million or more. Early-stage funding totaled $40.6 billion, up 38% from a year earlier, while seed funding reached $12 billion, rising 30% despite a decline in deal volume.

Despite the surge in private funding, public markets remained relatively subdued. The U.S. IPO market slowed during the quarter amid a broader selloff in software stocks. Globally, 21 venture-backed companies went public with valuations above $1 billion, with 17 listings occurring in Asia. The largest IPO was that of PayPay in Japan, a mobile payments fintech valued at $10 billion in the listing.

Mergers and acquisitions activity was stronger. Startup M&A deals totaled more than $56.6 billion, making it the third-highest quarter for such activity since the 2022 downturn. The largest deals were the $6 billion acquisition of ByteDance’s gaming platform Moonton by Savvy Games Group, and Capital One’s $5.15 billion purchase of fintech startup Brex.

Notably, unlike the cloud and mobile computing eras, this investment cycle buoyed not just software but also the physical world – with investments going to infrastructure, autonomous vehicles, robotics and manufacturing.