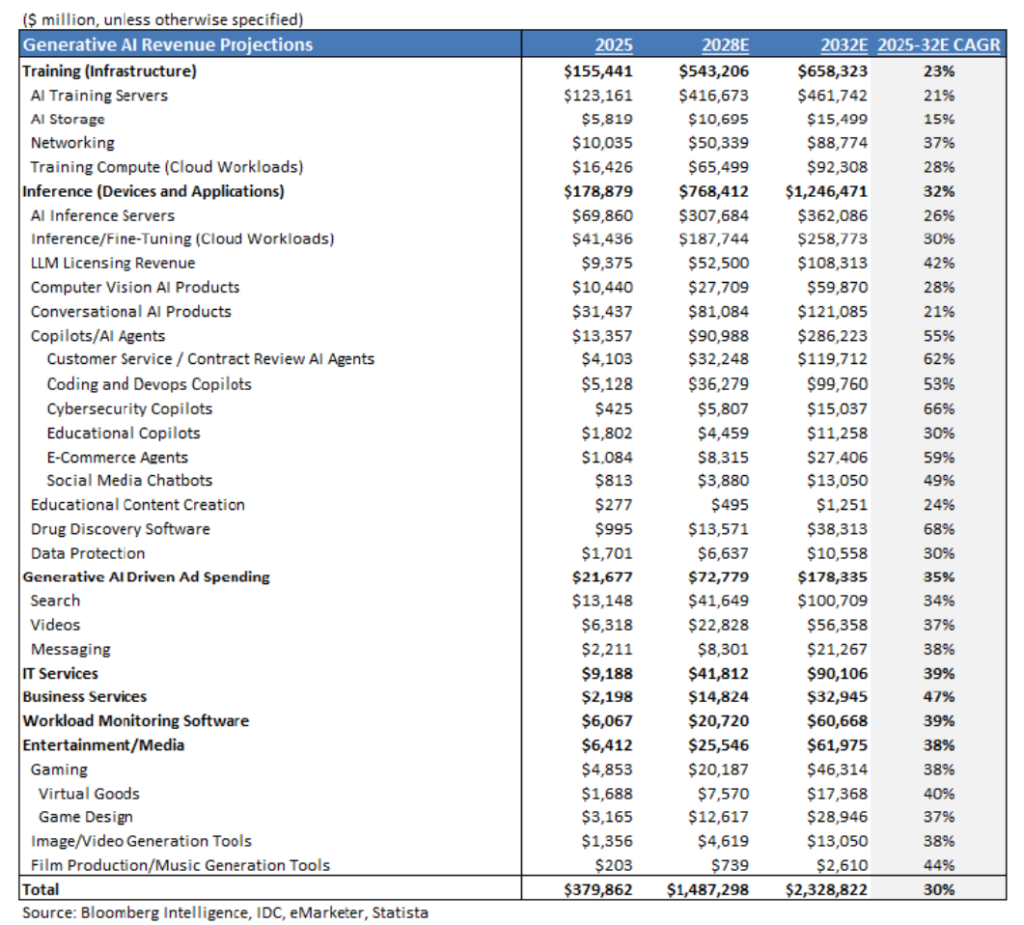

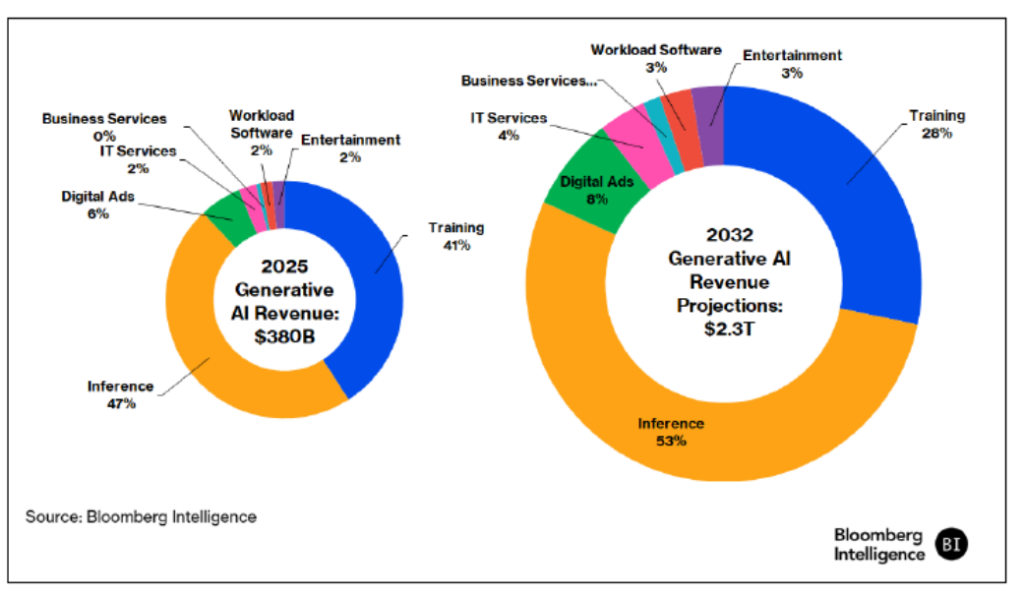

Bloomberg Intelligence expects generative artificial intelligence to become a $2.3 trillion market by 2032, with enterprise adoption increasingly shifting from building large models toward deploying AI agents and inference workloads that run them.

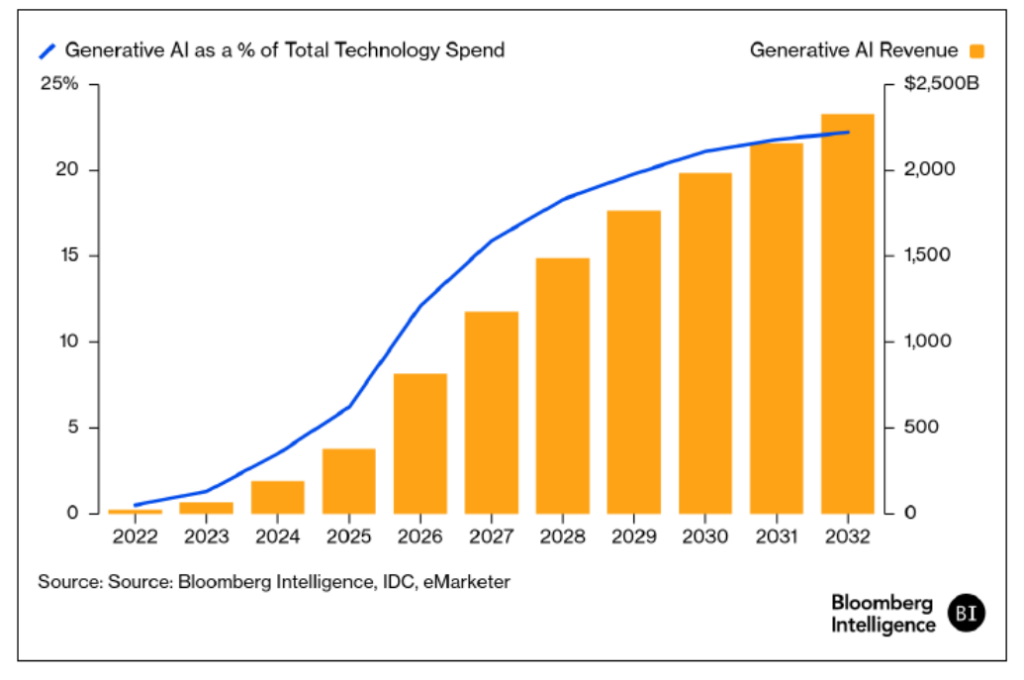

The forecast, detailed in the firm’s Generative AI 2026 Outlook, represents an increase from Bloomberg Intelligence’s previous projection of $1.8 trillion and reflects stronger-than-expected enterprise demand for coding assistants, AI agents and cloud-based AI services. The firm estimates AI-related spending will account for roughly 22% of all technology spending by 2032, up from about 6% today.

In an interview with The AI Innovator, Mandeep Singh, Bloomberg Intelligence’s global head of technology research, explains the basis of the projections. “When you look at the numbers underneath that headline number, inferencing is becoming a much bigger portion than what we originally thought.”

Need more clues? Ask the Sherlock chatbot in the lower right corner to summarize this story, explain technical concepts or answer other questions.

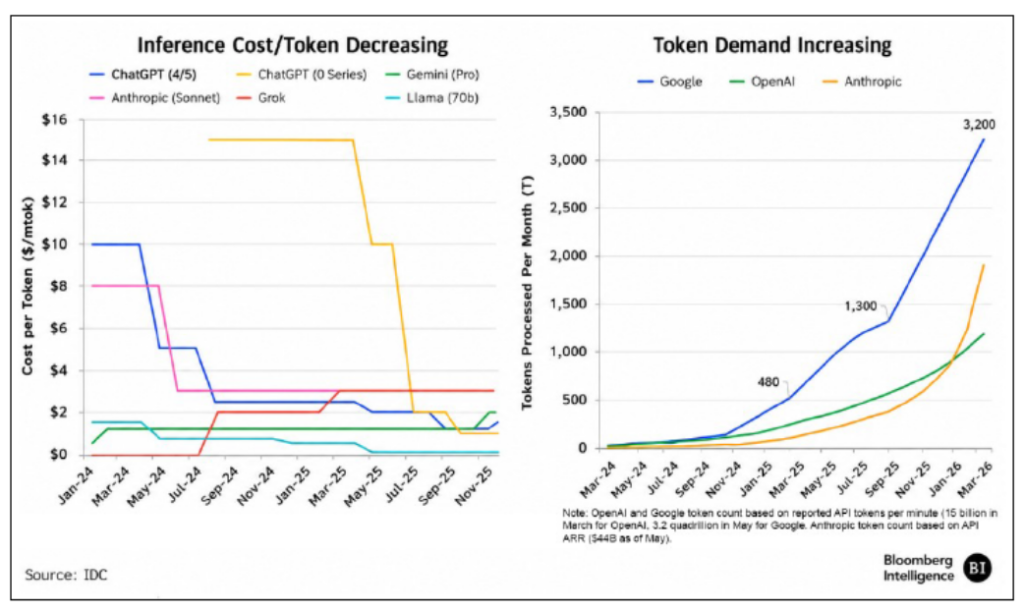

Rather than spending primarily on training ever-larger foundation models, enterprises are expected to devote increasing resources to inference — the computing required to run AI models in production. Bloomberg Intelligence now believes inference spending will surpass training several years earlier than it previously projected, driven by rapid adoption of coding agents and reasoning models.

The rapid growth in inference is “led by some of the prominent use cases like coding agents. The coding agent market is turning out to be a very big market, and we have put numbers around it in terms of how we expect that to grow,” he said.

Singh said reinforcement learning, enterprise fine-tuning and open-source models are changing how organizations deploy AI.

“There’s a lot more focus on fine-tuning the models using enterprise data, using techniques like reinforcement learning, and, in some cases, even using open-source models,” he said. “The whole idea is deploy AI while retaining your intellectual property around your data.”

Industries to see faster growth

The report identifies several areas expected to see the fastest growth over the next several years.

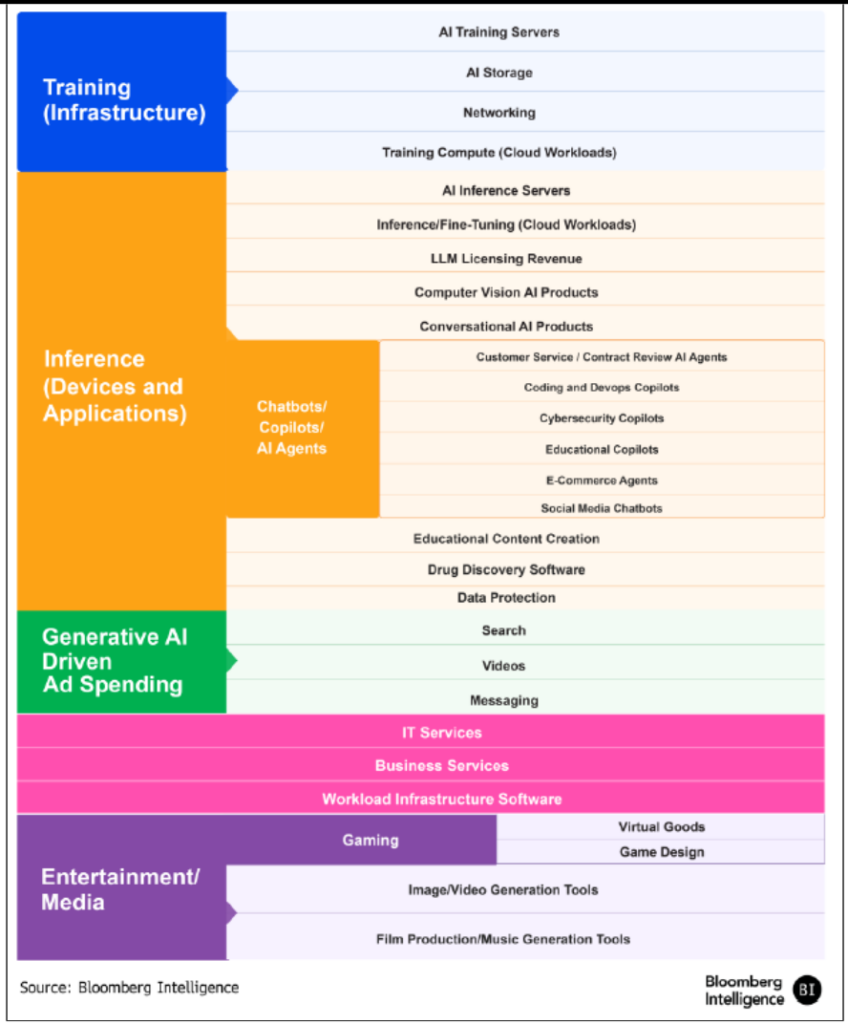

Among the strongest are networking infrastructure, inference fine-tuning, large language model licensing, coding agents, DevOps copilots and customer service AI. Bloomberg Intelligence projects coding agents and customer service agents will each become markets approaching $100 billion by 2032, while spending on AI agent products overall could reach about $286 billion – a compound annual growth rate of 55%.

As inference demand continues to surge, “cloud companies are big beneficiaries,” he said. On the flip side, however, “your SaaS (software-as-a-service) names would be the ones who would get disrupted from these coding agents, the customer service agents and other types of agents.”

Bloomberg Intelligence argues that hyperscalers and emerging AI cloud providers will own most of the AI infrastructure, while enterprises consume AI as a cloud service rather than build and operate large AI data centers themselves. It forecasts public cloud infrastructure spending could exceed $2.1 trillion by 2032.

Singh said economics favor cloud deployment for most organizations.

“When it comes to setting up these AI data centers, it’s going to be the hyperscalers, the neo-cloud vendors and, to an extent, some sovereigns,” he said.

Beyond infrastructure costs, he said the pace of AI model releases makes cloud deployment more practical because providers continuously update models.

“If you’re doing things on-prem, … how do you keep it up to date?” Singh said. “With cloud infrastructure, that’s the biggest advantage — they’ll keep it up to date for you.”

SaaS, IT and business services growth to slow

Bloomberg Intelligence is much less optimistic about traditional SaaS vendors.

While established SaaS companies are introducing AI products, Singh believes agentic AI will cannibalize their existing subscription businesses while simultaneously creating new AI-native competitors.

“The offsets from the agentic side would not be enough to get them to over 15% top-line growth as they were growing before,” he said. “Previously, it was a very simple, seat-based model and high renewals, so growing 15% to 20% was almost a given.”

“But now it’s going to be much tougher because of the cannibalization from agentic offerings of their existing products and the fact that there is more competition from newer vendors that are AI-native,” Singh said. “That’s going to be a challenge.”

The report also expects pressure on broader IT and business services as AI shortens software implementation projects and automates portions of application development.

Not in an AI bubble

Despite the rapid investment flowing into AI, Singh does not see today’s market resembling the dot-com bubble.

Unlike the internet boom of the late 1990s that went bust, AI spending is already producing measurable enterprise demand, particularly for cloud infrastructure and coding tools, rather than relying primarily on speculative future adoption, the analyst said.

The technology also has established revenue streams from hyperscalers, model providers and enterprise software vendors, making today’s investment cycle fundamentally different from the largely pre-revenue internet companies that characterized the dot-com era, according to Singh.

“You can draw some parallels, but I would argue that the presence of hyperscalers makes this quite unique. We’ve never had five or six companies with this kind of balance sheet and free cash flow ever,” he said, referring to companies including Amazon, Google, Microsoft and Meta. “They have the balance sheet to withstand big losses if that were to happen.”

So where should investors put their money today?

“The market is underestimating the strength and length of this cycle when it comes to the infrastructure build out,” he said. “If this is going to be a 100-plus gigawatt type of buildout, then we still have some room to go in terms of (investing in) the picks and shovels, semiconductors and semiconductor equipment” stocks.

Here are selected graphics from the report:

Generative AI Revenue Potential

Generative AI Spending

LLM Cost Per Token, Token Processed

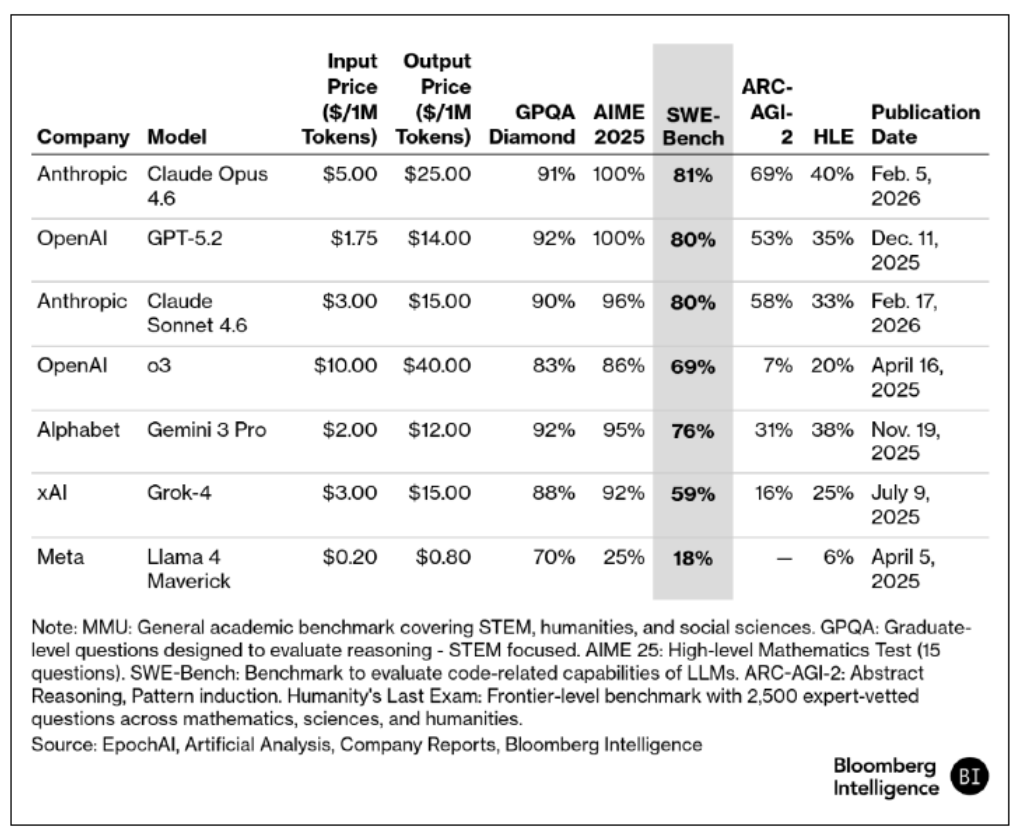

LLM Costs vs. Performance

Market Size by Deployment Type

Generative AI Market Overview

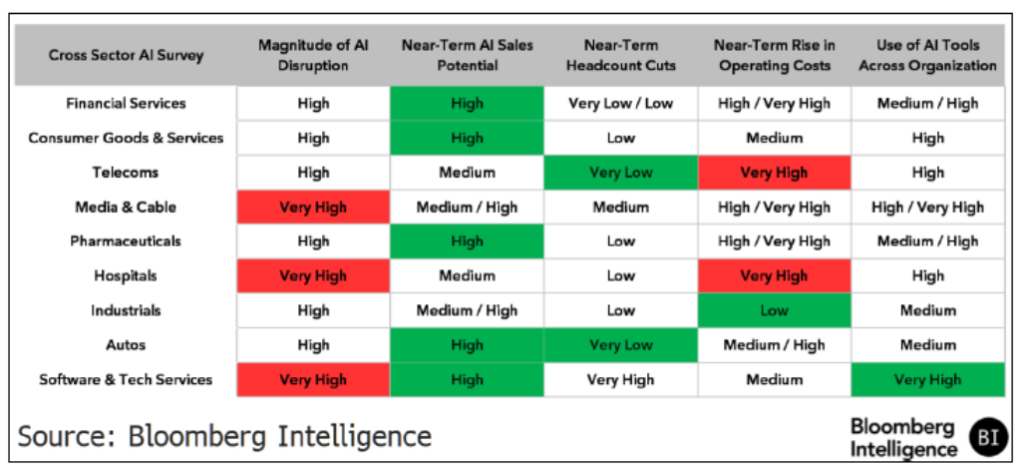

AI Industry Heat Map

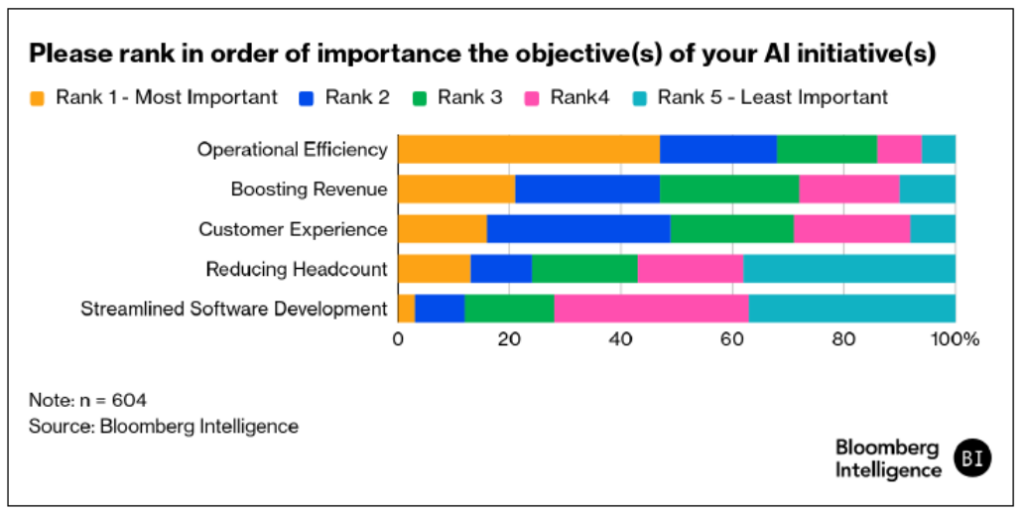

Survey: Ranking of AI Objectives